What are mortgage points and are they right for you?

Mortgage points are basically discount points. When you’re getting your home loan, you can buy mortgage points to lower your rate and save you interest in the long run.

The value of mortgage points are tied to market rates and conditions, which means they’re subject to change. In a volatile market, the value can change daily. Generally, you can estimate a point to be around 1% of your loan amount for a 0.25% rate discount, but your mortgage lending officer will advise you of the current climate.

Here’s How it Works

Here’s a simplified example of how mortgage points work to save you money:

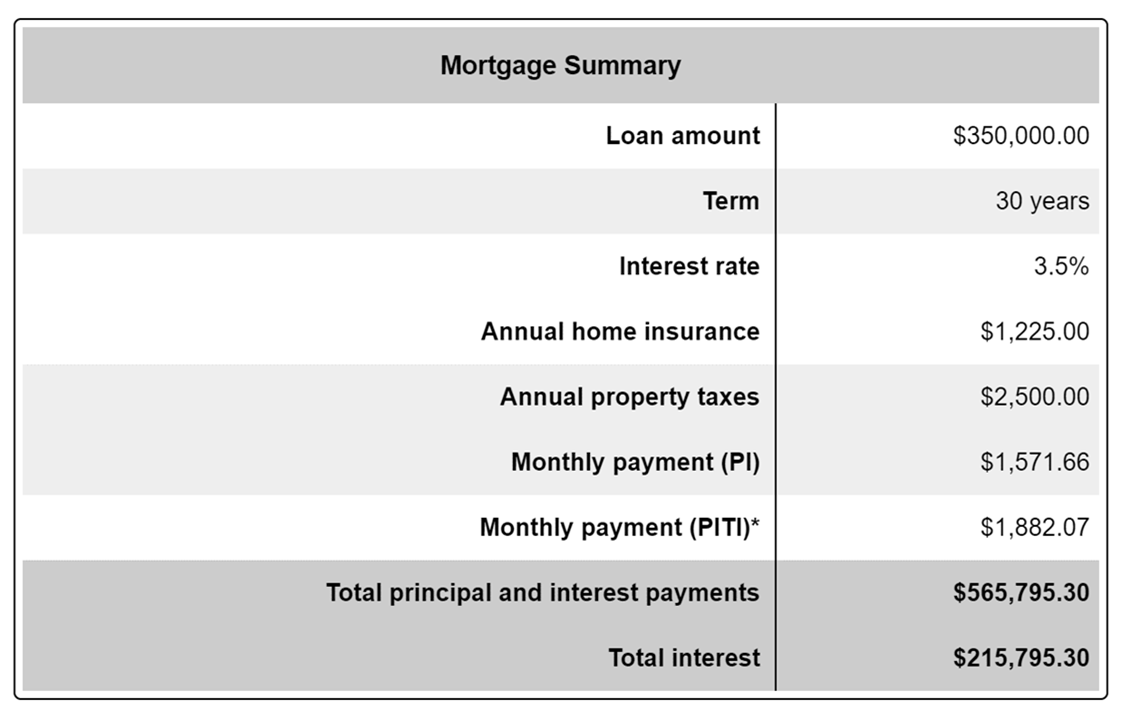

A member is getting a home loan for $350,000 with a 30 year mortgage at 3.5% interest. They can expect a monthly payment of $1,571.66. Over the course of their 30 year loan, they will pay $215,795.30 in interest.

The member is interested in buying mortgage points. They can buy down their rate approximately 0.25% by paying 1% of their loan amount for an up front cost of $3,500. This lowers their rate to 3.25% for 30 years. With the point, their monthly payment will be $1,523.22 and they can expect to pay a total of $198,360.37 in interest over 30 years.

So is the point worth it? It lowers the monthly payment by $48.44 and saves $13,934.93 (the difference in interest, minus the point payment) over the life of the loan.

This is great news if this member is buying their “forever home,” but what if they’re thinking of selling down the road? They can divide the cost of the point by $48.44 (the monthly savings) and see that the point pays for itself in six years. If the member is planning to stay in the home more than six years, the point is worth taking into consideration.

Why Not Just Pay More on the Down Payment?

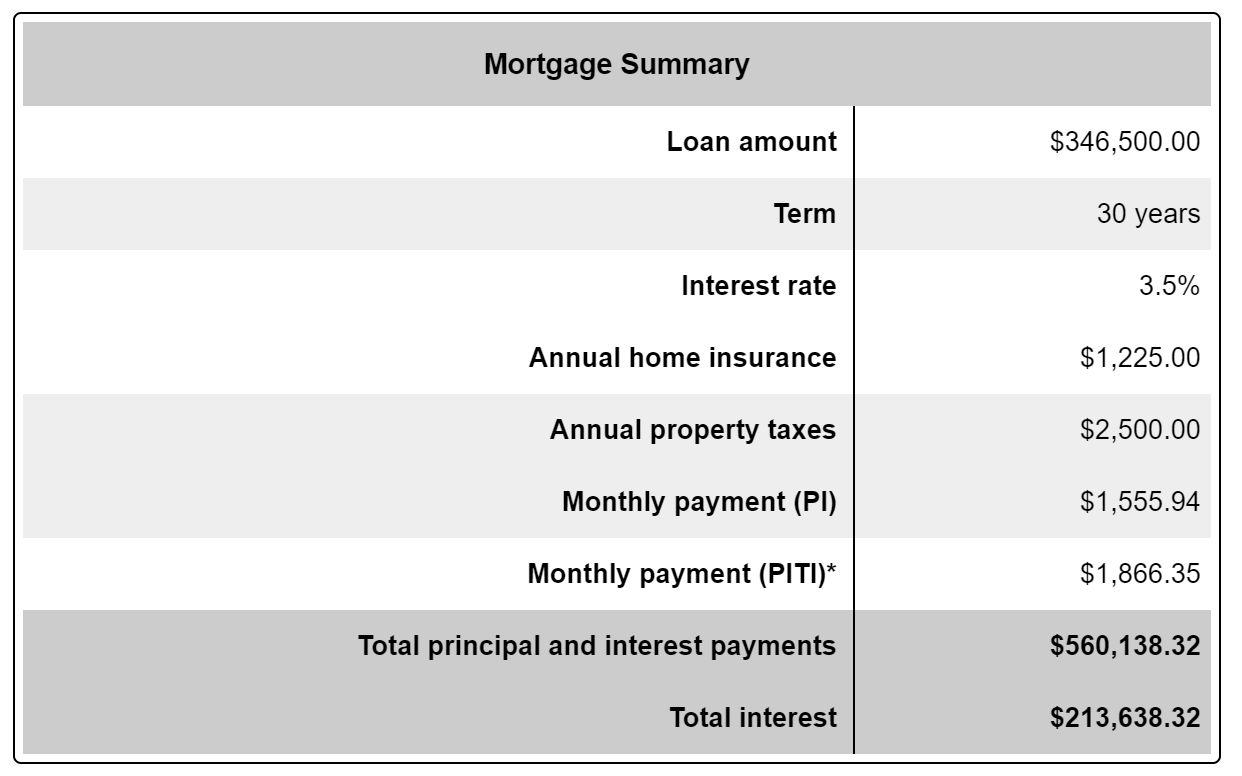

Here’s what it would look like if the member in our example put the additional $3,500 towards their down payment, bringing their loan to $346,500. They can expect a monthly payment $15.72 less than what they would pay financing $350,000 at the same terms, which saves $2,156.98 in interest over the life of the loan.

Want to Explore Your Options?

Buying a home is likely the biggest purchase you’ll ever make, which is why it’s so important to have someone on your team to advise you of all the financing options available to you.

SESLOC Mortgage Loan Officers can help you understand your options and find the solution that’s the best fit for your needs. For a free consultation, call (805) 543-1816, email or book an appointment.